यह भी देखें

25.06.2026 09:22 AM

25.06.2026 09:22 AMYesterday, US equity indices finished mixed. The S&P 500 fell by 0.10%, and the Nasdaq 100 dropped by 0.43%. The Dow Jones Industrial Average rose by 0.35%.

After Tuesday's large decline, global equities staged a recovery, and two powerful catalysts restored investors' risk appetite. A strong Micron outlook revived enthusiasm for AI, and Brent crude erased the war-related premium entirely. Nasdaq 100 futures jumped by about 2% today, S&P 500 futures gained roughly 0.6%, and South Korea's KOSPI surged by nearly 7%, recouping Tuesday's rout. Micron shares rallied by roughly 15% after the closing bell.

Micron's report delivered the loud end-of-season surprise the market wanted. The company guided to roughly $50bn in revenue for the quarter ending in August, versus a Wall Street consensus near $43.2bn, marking a very large beat. Demand for both traditional memory and high-speed memory for AI systems continues to outstrip supply, and Micron is using that deficit to lock in long-dated contracts, many stretching five years. That detail matters: Tuesday's sell-off was driven by fear the AI rally had gone too far and infrastructure investments would not pay off. Micron effectively answered that concern with five-year contracts that provide visibility on future sales.

Optimism quickly spread across the memory complex. SK Hynix said it plans to raise about $29bn via a US listing, and Japan's Kioxia — now its most valuable corp — also plans US-listed depository receipts. Both stocks jumped by roughly 15%.

At the same time, oil is writing a different story. Brent has fallen for a fourth session, slipping below $72.48/bbl, its pre-war closing level, which is a symbolic threshold. The entire price surge caused by four months of war and the closure of the Strait of Hormuz has now been fully unwound. As noted earlier, the restoration of flows through the gulf has proceeded faster than expected, evidenced by Qatari deals and renewed exports from the UAE, Iraq, and Kuwait.

The same dynamic has been bad news for gold. The metal continued to slide and fell below $4,000/oz for the first time since November. The logic is familiar: a strong dollar at a seven-month high and the prospect of Fed hikes squeeze a non-yielding asset. The pull-down has also hit miners' shares.

Bitcoin added about 1% but faces a large block of option expiries that could add downside pressure amid weakening institutional demand.

All eyes are now on today's release of the PCE price index, the Fed's preferred inflation gauge. Both the monthly and annual prints are expected to accelerate. If the data meets or exceeds consensus, the dollar should strengthen further, and risk appetite may cool.

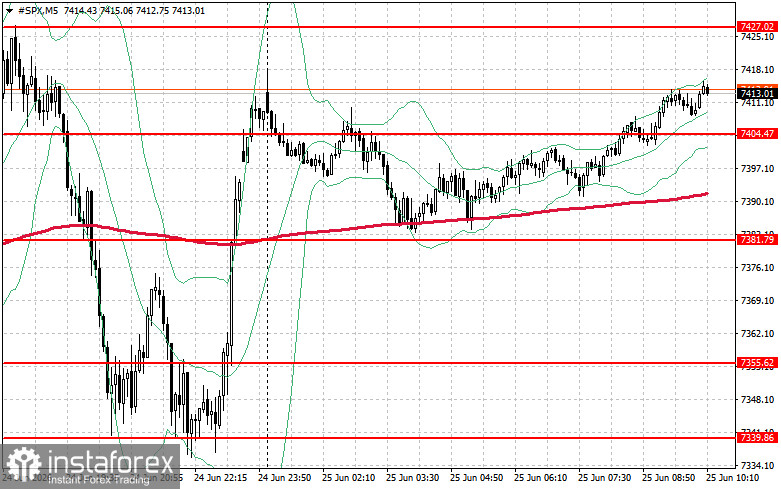

Technically, the S&P 500 analysis suggests that the immediate task for buyers is to overcome the resistance level of $7,427. Doing so would confirm upside and open the path to $7,451. Maintaining control above $7,474 would further cement buyers' positions. On the downside, buyers need to defend $7,404. A break below that level would likely push the index back to $7,381 and open the way to $7,355.